[ad_1]

If you’ve been researching mortgages, or are in the process of taking out a home loan, you may have come across the term “impounds” or “escrows.”

When you hear these seemingly complex words, the loan officer or mortgage broker is simply referring to an impound account, also known as an escrow account.

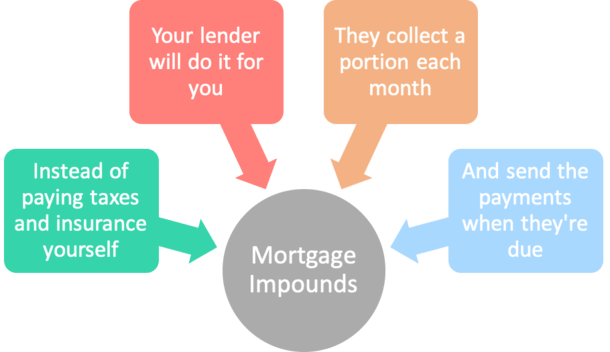

Here’s how it works. Each month, a portion of property taxes and homeowners insurance are collected along with your regular mortgage payment, then disbursed to the appropriate parties when due.

This arrangement ensures the lender that taxes and insurance are paid on time, instead of relying on the homeowner to make the payments themselves.

It protects the lender’s interest in the property since taxes are compulsory and insurance shields the collateral from harm.

What Are Mortgage Impounds?

- A housing payment includes a mortgage, homeowners insurance, and property taxes

- Impounds (or escrows as they’re also known) refers to the automatic collection of taxes and insurance

- It ensures the homeowner has funds available to make these important payments when due

- A portion of these costs is taken out of your housing payment each month and set aside until disbursement

Many mortgages these days require an escrow account to ensure the timely disbursement of property taxes and homeowners insurance premiums.

This account is managed by a third-party intermediary, typically a loan servicer, who collects and disperses funds on behalf of the homeowner.

Homeowners pay money into the escrow account at loan closing, and each month after that with their mortgage payment.

Over time, the balance grows and when property taxes and homeowners insurance are due, the money is sent on to the tax collector or insurance company, respectively.

Instead of paying property taxes twice a year, or homeowners insurance once annually, you pay a considerably smaller installment amount each month instead.

Along with each mortgage payment you also pay roughly 1/12 of the annual property tax bill and 1/12 of the annual homeowners insurance premium.

This is where the acronym “PITI” originates from – Principal, Interest, Taxes, and Insurance.

The taxes and insurance are paid in advance and the money is “impounded,” aka seized until being distributed. That’s where the name impound comes from.

And escrow simply refers to a third-party who holds the funds and directs them to where they need to go.

As noted, you must also pay an “initial escrow deposit” at loan closing, which will vary greatly based on the month you close, and where the property is located.

Lenders may also collect one or two extra months of payments to act as a cushion for future increases in taxes and insurance, but this amount is strictly regulated.

Why Mortgage Impounds?

- They basically exist to protect the lender from borrower default

- Assuming the homeowner falls behind on taxes or fails to make insurance payments

- The monthly collection of funds ensures the money will be available when payments are due

- And removes a situation where the borrower is unable to make what are often very large payments

An impound account greatly benefits the lender because they know your property taxes will be paid on time, and that your homeowners insurance won’t lapse.

After all, if you have to pay it all in one lump sum, there’s a chance you won’t have the necessary cash on hand.

Remember, the average American has little to no savings, so if a big payment is due, uh-oh!

Clearly this is important because the lender, NOT you, is the one that truly owns your home when you’ve got a giant mortgage attached to it.

And they don’t want anything to come in between the interest in THEIR property in the event you’re unable to make these critical payments.

Many seem to think lenders require impounds so they can earn interest on your money, but it’s really to protect their interest in the property.

*Also, some states require lenders to pay homeowners interest on their impound account balances anyway.

In California for example, it is customary for mortgage escrow accounts to earn interest. Each year you should receive a tax form that shows what you were paid and what you OWE as a result.

Be sure to check your own state law to determine if you’ll earn interest. In any case, it likely won’t be very much money, and it’s taxable…

Impound accounts can also benefit borrowers because the money is collected gradually over time, so there isn’t that big unexpected hit when taxes or insurance are due.

For this reason, some borrowers actually prefer impound accounts, especially those that tend to do a poor job managing their own finances.

And you shouldn’t miss a payment or pay late because it’s all done for you automatically. It’s actually pretty convenient.

[Homeowners insurance vs. mortgage insurance]

Paying Property Taxes and Homeowners Insurance Yourself

- You may have the option to pay these bills yourself as well

- But only on certain types of mortgage loans

- Such as conventional loans (conforming and jumbo loan amounts)

- Or on loans with a down payment of 20% or more

- But it may cost you .125% of the loan amount to waive them!

If you’re the type that likes full control over your money, you can always pay your property taxes and homeowners insurance yourself if the underlying loan allows for it.

In this case, you “waive impounds,” which usually entails paying a fee to the lender, such as .125% or .25% of the loan amount at closing.

For example, if your loan amount is $200,000, you might be looking at a cost of $250 to $500 to remove impounds. It’s not insignificant.

Or, waiving impounds/escrows may come in the form of a slightly higher mortgage rate if you don’t want to pay the escrow waiver fee out-of-pocket.

Either way, there is typically a cost, though you can always try to negotiate your mortgage rate with the lender to get them waived and still secure a low rate.

Just keep in mind that you can’t always waive impounds depending on loan type.

Impounds are required on FHA loans, VA loans, and USDA loans.

For conventional loans, impounds are generally required if you put less than 20% down, which is the case for most borrowers.

And even then, many lenders charge borrowers if they want to waive impounds, despite their loan-to-value ratio being super low.

In California, impounds are technically only required if the loan-to-value ratio (LTV) is 90% or higher. But you may still have to pay to waive them either way.

It’s seemingly unfair, but like all other businesses, they got creative and came up with yet another thing to charge you for. Sadly, you should be used to this by now.

How to Remove Mortgage Impounds

- You can request the removal of impounds once your LTV is at/below 80%

- Either by paying down your loan over time or via lump sum payment

- But there’s no guarantee the lender will agree to do so

- It’s still a voluntary decision on their part to remove them at your request

If you initially set up an escrow account, you may be able to get it removed later down the line.

Simply contact your loan servicer and ask them to review your escrow account.

As a rule of thumb, your request is more likely to get approved if your LTV is at or below 80%. That way they know you’ve got skin in the game.

That 20% in home equity gives the lender sufficient protection from potential default if you fail to pay property taxes or home insurance in a timely fashion.

But it’s not a guarantee for removal. Sometimes they’ll simply balk at your request, even if you have a ton of equity.

Also note that if you have an escrow account and refinance your mortgage, the money should be refunded to you within 30 days of paying off your old loan.

The Annual Escrow Analysis

- Loan servicers are required by law to review your escrow account annually

- This happens once a year on your origination date to ensure it’s balanced

- If you paid too much you may receive an escrow surplus refund check

- If you didn’t pay enough you may need to pay an escrow shortage

Each year on the anniversary date of your loan closing, your lender is required by federal law to audit your impound account and refund any excess over the allowable cushion.

You will also receive an escrow analysis statement that can be handy to look over.

Generally, the minimum balance required for an escrow account is two months of escrow payments, which covers any increases in taxes and insurance.

When your loan servicer projects the numbers for the year ahead, any surplus, which is your estimated lowest account balance minus the minimum required balance, will be refunded to you.

If your account balance is higher than this minimum amount, you may be refunded the difference via check. It’s a nice surprise when it comes in the mail!

Assuming you aren’t just sent a check that can be cashed, you may get the option to apply any overage to principal reduction or to a future mortgage payment.

You can also be proactive if it appears as if your impound account is a little too full. Simply call and ask them to take a look via an escrow account overage analysis.

Conversely, it’s possible that you may experience an escrow shortage, in which case you’ll be billed for the amount needed to satisfy the shortfall.

While not as nice as a check, it indicates that you haven’t been overpaying throughout the year.

The loan servicer may also give you the option to accept a higher monthly payment going forward to catch up on any shortage.

Note that both an escrow account surplus and shortage can result in a different monthly mortgage payment, since they will collect more or less from you in the future.

For example, if you were paying too much last year, you might be told that your new monthly payment is X dollars less. Your mortgage payment went down. Another unexpected surprise!

If you were paying too little, the reverse might be true – your mortgage payment may go up!

However, the difference will typically be quite small relative to the overall payment.

It’s Always Your Responsibility to Pay on Time

- Regardless of how you pay taxes and insurance

- It’s always your sole responsibility to ensure they’re paid on time

- You can’t necessarily blame the mortgage lender/servicer if they slip up

- So always follow up to make sure the payments are made on time

Regardless of whether you go with impounds or decide to waive them, it is your responsibility to ensure that your property taxes and insurance are paid on time, each and every year.

Sure, your loan servicer will probably pay on time, but this may not always be the case. Mistakes happen.

Also, if you’re subject to paying supplemental property taxes, your loan servicer may tell you that it’s your responsibility to take care of them on your own.

If you receive a supplemental property tax bill in the mail, you may want to call your servicer immediately to determine if it will be paid via your escrow account. If not, you’ll need to send payment yourself.

Situations like these are a good reminder to always keep an eye on your escrow account, and to keep solid records of your taxes and insurance.

In summary, it can be nice for someone else to handle these payments on your behalf, but you still have to make sure they’re doing their job!

Pros and Cons of an Impound Account

The Pros

- No surprise tax/insurance bill every six or 12 months

- Taxes and insurance are paid gradually throughout the year

- Easier to create a budget and manage other expenses

- Better idea of how much house you can really afford

- Don’t have to physically make the tax/insurance payments yourself

- No fee (or mortgage rate increase) for the removal of impounds

The Cons

- Your mortgage payment will be higher each month

- Less liquidity because money is being held in escrow

- Could be using that money in other ways and potentially earning a higher return

- Loan servicer could make a mistake while making payments on your behalf

- Have to deal with your mortgage payment changing annually

(photo: Constantine Agustin)

[ad_2]

Source link